High-functioning businesses can thrive even in dysfunctional environments – as success stories from South Africa show.

It’s tough to make predictions, especially about the future,” quipped the mid-20th century American baseball star Yogi Berra. Uncertainty is an inherent aspect of the human condition – and the more we attempt to control outcomes, the more we come to realize that truth. As Nassim Nicholas Taleb wrote in his bestseller from the era of the global financial crisis, Fooled by Randomness: “No matter how sophisticated our choices, how adept we are at manipulating the odds, randomness will always have the final say.” There is no doubt that an unpredictable and rapidly changing global environment has made the task of managing companies and the people that work in them increasingly complex.

Leaders are required to make decisions based on imperfect information every day and, despite our increasing use of data and analytics, that is not going to change. What is changing is the volume and velocity of information you need to process in order to chart a course in a world where multiple crises have not only exposed serious fault lines in many economies, but have aggravated numerous global structural problems.

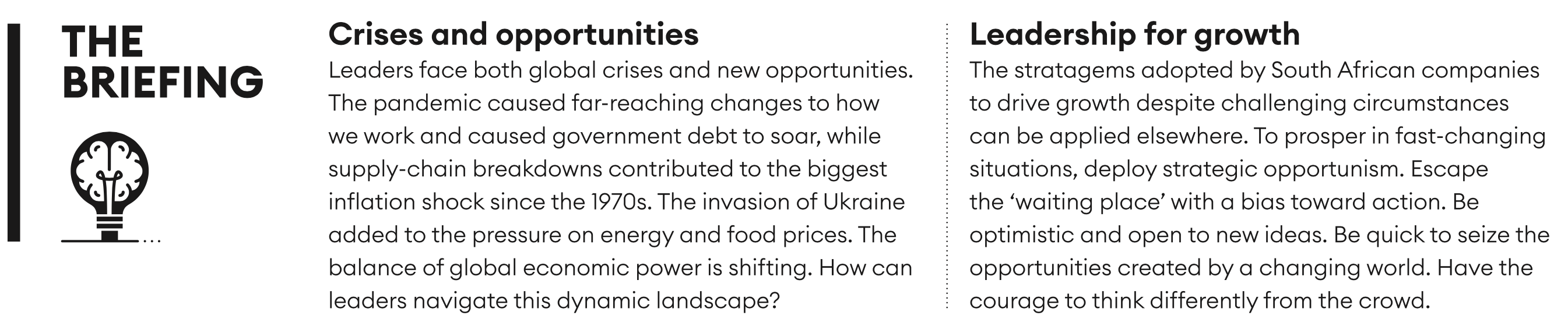

Global crises and new opportunities

Had someone told you at the beginning of 2020 that the world was on the brink of a global pandemic that would lead to governments confining entire populations to their homes to limit the strain public healthcare systems; that wealthier nations would deliver the biggest stimulus packages in history as millions lost their jobs, causing government debt levels to balloon to a record $307 trillion according to the Institute of International Finance; and that this would coincide with a breakdown in global supply chains, resulting in the biggest inflation shock since the 1970s; you might have questioned their judgment.

Had they then added that Russia would invade Ukraine, causing further rises in global food and energy prices, exacerbating the worst cost-of-living crisis in generations, you would have been perfectly within your rights to recommend they go for a long lie-down in a dimly lit room with a damp cloth on their foreheads.

On top of this, there are significant shifts in global power dynamics which are causing anxiety in the boardrooms of many highly developed economies. Emboldened by the rapid growth of their economies over the past two decades, the so-called Brics countries – Brazil, Russia, India, China and South Africa – are leading the most concerted effort since the Cold War to challenge the US-led multilateralism that has defined the rules of international engagement since the end of World War II. Thanks to sustained growth in many emerging economies, led until recently by China and now increasingly by a resurgent India, Brics countries now account for 32% of global GDP, against the G7’s 30%. Whether Brics will ever evolve to anything more than a select members club of disparate nations that occasionally collaborate (but only when it serves their narrow self-interest) remains unclear. But their increased economic heft is undeniable – and their ongoing growth presents huge new opportunities for those who are open to them.

It’s good to be prepared for multiple eventualities, and taking lessons from one of the most hostile business environments on Earth may help you in that process. I have spent the last 20 years studying top-performing companies in South Africa and have distilled the key lessons in two books since 2020: The Upside of Down and Genius: How to Thrive at the Edge of Chaos. The South African economy has been in steady decline over the past 15 years. The country was headed for trouble before the onset of the global financial crisis: the Mandela magic was fading and, after 14 years of steady expansion, that crisis coincided with a series of disastrous domestic events. The country’s ongoing electricity crisis began at that time, as did an extended period of political upheaval which has seen many key state institutions hollowed out.

During that time, GDP per capita shrank by an average of 0.34% a year. However, the profits of the country’s top 40 companies rose at an average of 7.6% a year, leading to a doubling of the valuation of shares listed on the Johannesburg Stock Exchange, despite a near halving in the number of listings (due mostly to private equity activity and some corporate consolidation). Why that apparent contradiction? How is it possible for so many high- functioning businesses to thrive in a largely dysfunctional environment?

It is largely down to a key leadership characteristic: sagacity, which is the quality of having keen discernment, sound judgment and the ability to make wise decisions based on experience and understanding. While Yogi Berra was right about our inability to predict the future, I have seen first-hand that leaders can chart a prosperous course in uncertain times. There are few things that focus the mind more sharply than operating in an unpredictable environment. Here are some of the behaviors that make the difference.

Strategic opportunism

Succeeding amid endemic unpredictability takes what former Harvard professor Daniel Isenberg defined as “strategic opportunism”. For organizations to survive the turbulence that is coming, they must remain open to seizing unexpected opportunities that align with their long-term goals and objectives, even if these were not part of the original plan. It involves flexibility in decision-making and the ability to adapt to changing circumstances in order to gain competitive advantage where rivals might be reluctant to act.

This requires leaders to be optimistic about the future. That doesn’t mean having an unwavering sunny disposition – rather, the firm belief that the future will be better than the present and they are in a position to drive positive outcomes. In a world awash with conflicting and often weaponized information, the most effective leaders sift through the clutter and assess what to eliminate, choosing to focus on the things they can influence and navigating the rest.

Escaping the waiting place

“If it’s not Armageddon, you must be building,” says Adrian Gore, the founder and CEO of Discovery Holdings, an insurance company started in 1992 as a provider of innovative private health cover. Today its shared-value insurance model, which incentivizes its clients to live healthier lives, is present in more than 30 countries, covering 40 million lives, in partnership with some of the worlds’ biggest insurers, including AIA in Asia, Ping An in China, Generali in Europe, Sumitomo Corp in Japan, Manulife in Canada, and its wholly owned subsidiary, Vitality Health & Life, in the UK. Gore is an unexpected proponent of the lessons from Dr Suess’s 1990 New York Times bestseller, Oh, the Places You’ll Go! The book’s main protagonist recognizes he cannot be constrained by the indecision he witnesses in those trapped in the dreaded “waiting place”, where they languish, looking for signals about where to go and what to do next. Gore is adamant that all the problems that companies (and indeed countries) face can be resolved by ensuring the right people in the right teams make the right decisions, and execute on their agreed strategies quickly and efficiently.

Optimism and openness

“Most people miss opportunities because they come dressed in overalls and look like work,” quipped inventor Thomas Edison. He showed the power of persistence in the continuous and relentless improvement of his ideas – and it takes a particular brand of optimism to not give up when the going gets tough.

There is a wonderful simplicity to the approach taken by Piet Mouton, the chief executive of investment firm PSG, which has a 30-year track record of superlative capital allocation, when he says: “Negative people never build anything.” Growth demands optimism and an openness to new ways of doing things.

PSG’s most successful investment is Capitec, which remains the fastest-growing retail bank in Africa more than two decades since it was founded to serve a mass market deemed by established legacy banks as ‘unbankable’. (See Dialogue Q2, 2023, to catch up with Capitec chief executive Gerrie Fourie in a previous interview.) Through its creative approach to that segment of the market, Capitec has built a highly profitable base of 20 million retail customers.

Seize the opportunities created by a changing world

For those operating in developed economies, it sometimes seems that there are fewer game-changing opportunities than in the fast-changing world of the Brics and other developing markets. But as the boom in technology has shown us over the past two decades, the worlds’ best opportunities are often hidden in plain sight. As economic power shifts steadily, those open to opportunities will spot them quicker than others.

Long before it became the second biggest brewer in the world, SABMiller, trapped in its home market due to global sanctions against apartheid South Africa, knew two things about the future. First, that the race-based ideology that excluded black South Africans from opportunities in their own country would come to an end; and second, that countries in Eastern Europe which

had remarkable but neglected heritage beer brands would open up to investment with the fall of communism.

It spent a decade refining systems, processes and people to capitalize on what it knew would be a once-in-a-lifetime opportunity for extraordinary growth. When both of its key scenarios occurred simultaneously, the firm was ready for the growth which made it a dominant global player, eventually being subsumed in Anheuser-Busch Inbev. (It was, at the time, the biggest corporate takeover on the London Stock Exchange.) SABMiller’s biggest strength was that it never descended into self-pity or complacency: instead it prepared itself for a once-in-a-lifetime opportunity, which it exploited with precision.

Resist the retreat into survival mode

“It’s much easier to find opportunities when times are tough,” Investec co-founder Stephen Koseff told me. “If it’s in your patch and someone gets into trouble, it can provide an opportunity.” But, beset by their own challenges, few companies have the confidence to seize those opportunities.

Investec grew from a small Johannesburg financial services firm to a top-ten wealth manager in the City of London in just over a decade, by doing multiple strategic acquisitions (some admittedly more successful than others). Koseff operated on the basis that deals were cheaper to do when times were tough and there were fewer competitors for assets. Most companies make the mistake of parking long-term strategy in times of uncertainty. They are so busy coping with the immediate threats that appear from every angle that they go into survival mode.

This is where strong teams are critical. I once asked South African businessman Laurie Dippenaar his greatest learning from three decades of growing Africa’s most valuable banking group, FirstRand. Famous for his ability to simplify complex concepts, Dippenaar explained: “When we had to make a big decision, we got our most talented people around the table, and whoever brought the best facts to the table and argued those with conviction would carry the day. Once we agreed on a course of action it was everyone’s job to implement the decision in their own departments.”

It is also leaders’ job to identify opportunities, even while growth in many economies remains uncertain. Inaction in difficult times is tantamount to going backwards. The challenge today is to find innovative and creative ways to lead in a decade where the average cost of capital will be higher than the 10 years previously, where workers are rattled by the threats of disruption driven by new technologies such as AI, and the relative post-war peace and stability enjoyed by the baby-boomer generation is by no means guaranteed.

By learning some lessons from those able to grow in deep dysfunction, today’s leaders need to cast the net wider in terms of finding new growth opportunities. It all begins with having the courage to think differently from the crowd.